As cashless payment becomes more widespread in Colombia, problems are starting to emerge. Can creaking infrastructure and systems handle the demand?

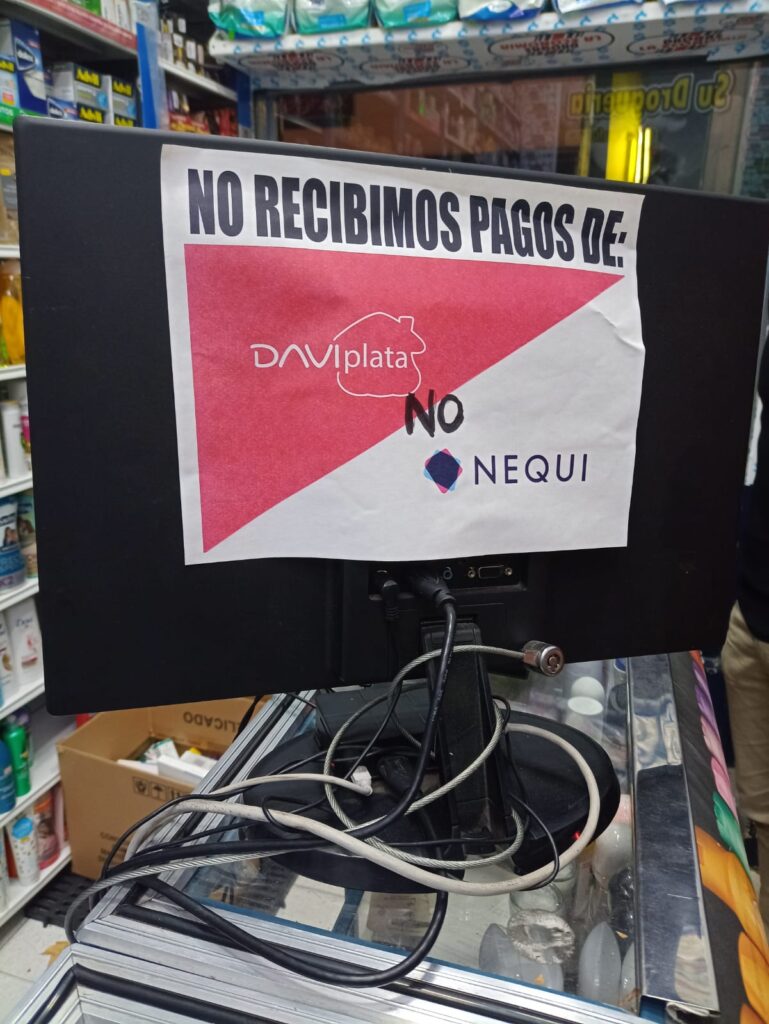

“The system collapses too often,” says Andrea at my local drugstore, “and it’s a really fastidious process to get the money back.” She is explaining why she is refusing payments made via the Nequí platform.

Founded by Bancolombia in 2016, Nequí was originally a way to give unbanked people a leg up into the formal financial system. Unlike traditional banks, it didn’t require going into bank branches, nor a lengthy list of documents to register. It was also digitally native.

This is part of a wider trend known as neobanking. These are less banks as you may know them and instead fintech. They offer fewer services and tend to focus on previously unbanked people outside the traditional financial landscape.

The big beast of the Latin American scene, Brazil’s Nubank, is already here in Bogotá and winning over thousands of people with its offers. Chief among them is the promise of high interest rates on ordinary accounts. That still runs around 8% APR, and was closer to 12% at first.

Nequí alone has some 20 million regular users – about half Colombia’s adult population. Three quarters of those are 45 or under, with the majority under 25. It’s no exaggeration to say that these platforms have completely changed the financial landscape of the country.

However, 80% of day-to-day purchases in Colombia are still made using cash. There are all kinds of reasons why the establishment would like that to be reduced, chief among them the fight against fraud and corruption.

This is part of a wider trend in Colombia to move towards a more modern banking system and break up the powerful and conservative banking blocs. Last year, the central bank (Banco de la República) brought in the Bre-B system of inter-bank transferrals to make them immediate rather being delayed often up to three working days. Banks are slowly moving onto it.

Why are some establishments rejecting the apps?

Put simply, it’s a lot of hassle for them and not always reliable. Like many tech companies, fintech operations are generally more focused on disruption than creation, meaning that they do not prioritise ongoing customer care.

Neither do they use their own infrastructure, relying instead on the existing systems – which is one of the key points of failure. Even in central Bogotá, both electrical and telecommunication connections can be extremely ropey.

For the electrics, there is the ever present threat of severe storms affecting things, as well as criminal groups cutting cables to extract the copper – more widespread than you might assume.

For the internet connection there is that, plus the added effect of extreme strain on the system. There are eight million odd people in Bogotá, most of which are heavy mobile phone users. It’s somewhat of a miracle we ever have signal.

More controllable for the fintech companies is their end, but they have problems there too. Server space is necessary to handle all this data, and a never ending stream of tiny payments requires a lot of processing power. A team of developers is needed to fix gremlins in the system.

For companies constantly looking to cut costs to stay competitive – few of the neobanks offer low-risk, high-return instruments such as mortgages – the temptation is always there to skip investing in emergency mitigation measures.

Even a simple money transfer requires a fair bit of coverage – there needs to be power at both the banking and retailing ends, as well as internet access at both points and space on the server to handle it all.

Added to this is growing concern over the potential for estafas, or scams. These are not commonplace yet on these platforms, but that’s largely a product of novelty. The more widespread the apps become, so too will an industry of fraudsters and scammers pop up.

How common is cashless payment in Colombia?

These payment systems are not simply found in flashy neighbourhoods – you are in fact more likely to pay via Nequí for a fruit juice in somewhere like the Honda plaza de mercado. It can be done via QR code or as a sort of mini-transferral.

That’s really the key to these new payment methods – they offer a democratization of payment methods through the one thing that almost all Colombians have nowadays: their phone. The same is true of cash, of course, but that can be fiddly and more theft-prone. After all, you can’t block your cash.

Through these platforms, you also have the chance to take out micro- or even nano-credits, avoiding the need to use informal gota a gota loans. These have grown in popularity recently and are simply put, traditional loan sharks with exorbitant rates of interest and credible threats of violence if payments are not met.

Bitcoin has yet to truly take off, but undeniably lies on the horizon. Medellín has a fair few places that will accept it and some parts of Bogotá will as well. It remains a novelty for the time being, but a chronically weak peso means that many are looking for alternative forms of keeping money.

Will cashless payment in Colombia grow?

Undoubtedly. There are serious issues to get over, but the rest of the world is trending heavily towards cashlessness and there is no reason to imagine that Colombia will not go exactly the same way.

As the popularity of cashless payment in Colombia rockets, it’s starting to put more and more pressure on a lot of interconnected systems. There have long been gripes over successive governments refusing to invest in infrastructure and this is simply one more symptom of chronic underfunding.

However, this is a house that Colombia simply has to get in order. The future is clearly cashless and it is already causing friction in the hospitality industry. Many foreign tourists simply cannot understand why cash is still a thing and are irritated by having to withdraw and cart around notes and coins.

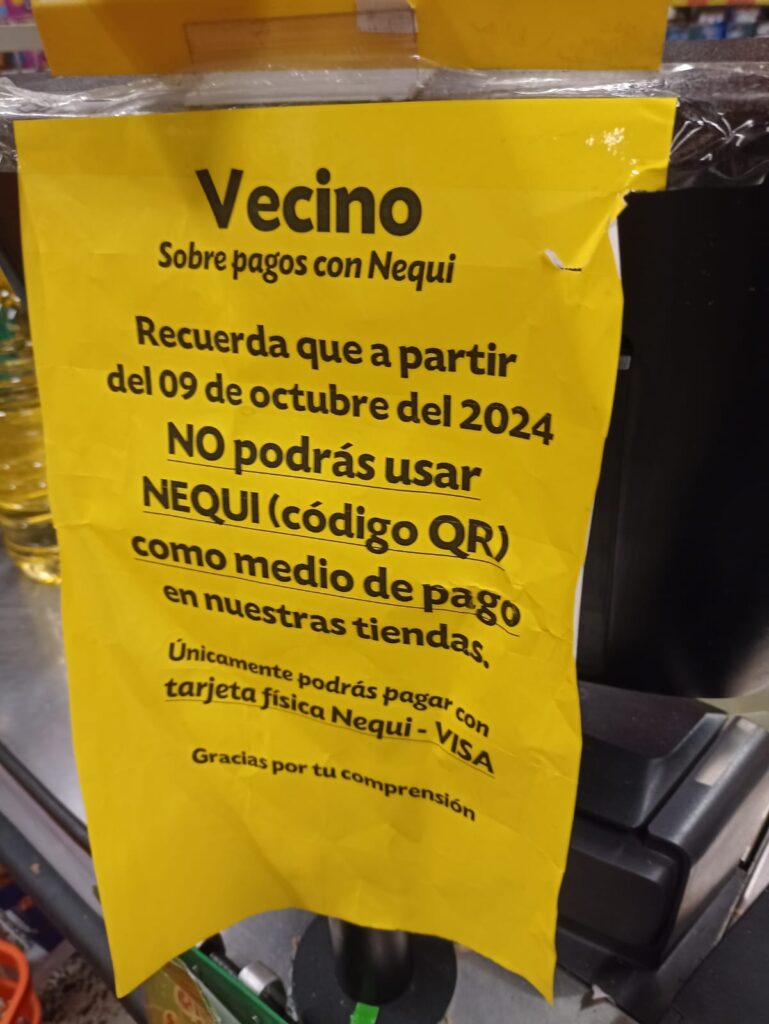

It’s likely that the country will switch to a more traditional form of cashlessness, with digital QR codes already being retired by Nequí in favour of migrating people towards their new Visa card (digital and/or physical). These are usually seen as more stable and reliable.

So cashlessness is coming, even if it might be slow to arrive fully. Just like the paperless office, the future often seems like it’s never going to be here until suddenly one day it is.